In mid-July 2025, Nvidia announced it expected to resume sales of its H20 AI accelerator to China after the U.S. government signaled it would grant the necessary export licenses, reversing a restriction that had frozen those shipments only months earlier. That single policy swing did not just move Nvidia’s stock. It exposed how quickly the ground under your infrastructure procurement can shift when a chip, a license, or a vendor roadmap becomes a geopolitical instrument overnight.

For US mid-market IT leaders, the temptation is to file this under “big-tech news that does not touch me.” That instinct is wrong. The same forces that let Washington restrict, then unrestrict, the flow of AI silicon to China are the forces that determine what hardware you can buy, when you can buy it, what it costs, and how long your current platform stays supported. The lesson of the AI export restriction is not about China. It is about volatility, and about who absorbs it.

The pattern deserves attention precisely because it is not unique. In the span of three years, mid-market technology buyers have absorbed pandemic-driven component shortages, the semiconductor lead-time crisis that pushed server delivery windows past a year, a wave of licensing model rewrites, and now a policy environment where the rules governing the most strategic silicon on the planet can flip in a single quarter. Each of these events arrived without warning, each landed on budgets that had been built on the assumption of continuity, and each rewarded the organizations that had designed for change over the ones that had planned for stability. The AI export restriction is simply the most recent, and clearest, entry in that ledger.

The AI Export Restriction, in Plain Business Terms

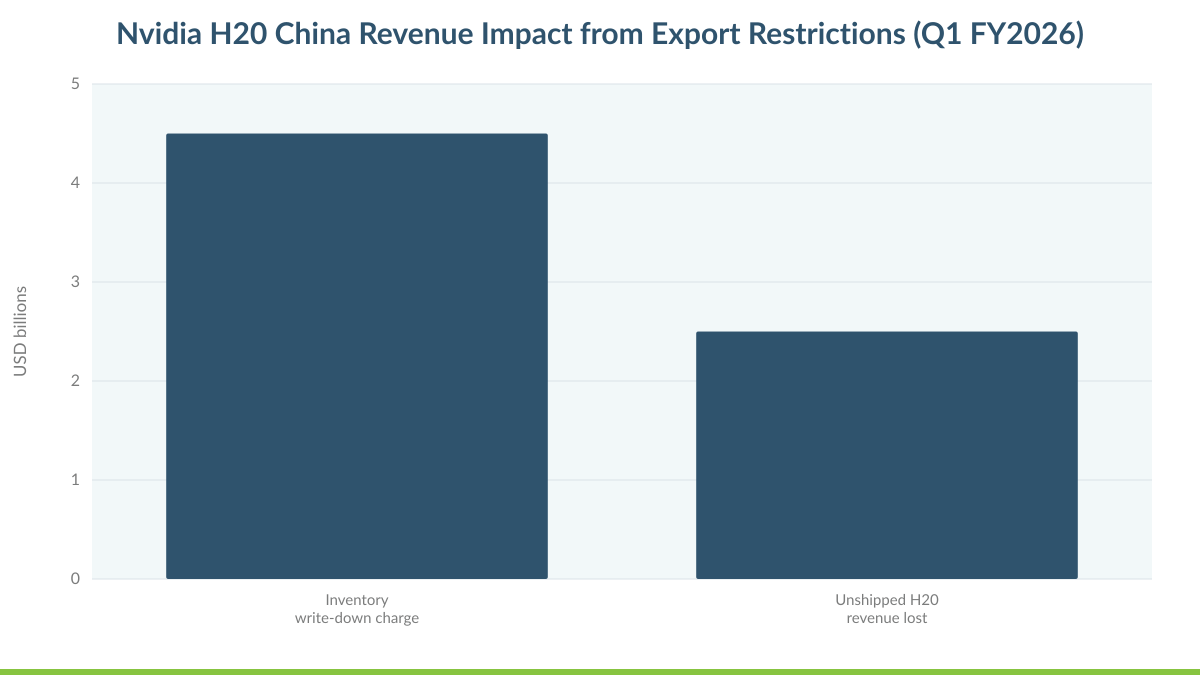

Here is the sequence stripped of jargon. In April 2025, the U.S. tightened controls on the Nvidia H20, a chip Nvidia had specifically designed to comply with earlier restrictions on selling advanced AI hardware to China. The tightening effectively banned the H20 from that market without a license. Nvidia disclosed in its Q1 fiscal 2026 filing that the move carried a multibillion-dollar cost, including charges tied to inventory and purchase commitments it could no longer fulfill. Then, roughly a quarter later, the policy reversed and licensed sales were back on the table.

The H20 itself is worth understanding, because it illustrates how fragile a compliance-driven product strategy can be. Nvidia did not stumble into the restriction. The company engineered the H20 specifically to sit under the performance thresholds that earlier export rules had drawn, a deliberate act of designing to the rules as they existed. When the rules moved anyway, that engineering investment was stranded overnight. A product built to comply with one version of policy became noncompliant under the next. For any buyer, the takeaway is uncomfortable: even a vendor with vast resources and direct visibility into the regulatory conversation could not design its way to certainty. If Nvidia cannot lock down the rules, a mid-market IT team certainly cannot.

The chart above, drawn from Nvidia’s own Form 8-K for Q1 fiscal 2026, shows the scale of the revenue impact and charges the company absorbed when the H20 was blocked. This is not an abstraction. When a single product line generates billions in exposure from a rule change, every downstream buyer of compute inherits some fraction of that instability in the form of pricing, availability, and roadmap uncertainty. The AI export restriction is a case study in how fast a durable-seeming supply chain can be re-drawn.

The AI export restriction is not a story about China. It is a story about how quickly the ground under your infrastructure procurement can move, and who is positioned to absorb the shock when it does.

Mid-market organizations rarely buy H20-class accelerators directly. But the ripple effects reach you anyway. When the highest-margin, highest-demand silicon gets caught in policy crossfire, manufacturers reallocate capacity, resellers reprice, and lead times stretch. The GPU you wanted for an internal AI pilot, the server refresh you budgeted for eighteen months out, and the licensing terms attached to your virtualization stack all sit downstream of decisions being made in Washington and in vendor boardrooms. Treating procurement as a purely technical exercise, disconnected from policy risk, is how mid-market IT budgets get ambushed.

Consider the mechanics of that ripple in a specific case. A regional healthcare provider or a mid-sized manufacturer planning an AI-assisted analytics workload does not sit at the front of the allocation queue. When a dominant vendor reallocates fabrication capacity to serve either a restored export market or the hyperscalers who buy in tens of thousands of units, the mid-market order slips down the priority list. A quoted lead time of eight weeks becomes twenty. The capital expenditure that was approved in one fiscal cycle now spans two, and the project’s return on investment erodes while the hardware sits on a manifest somewhere. The restriction did not target that buyer, yet the buyer pays for it in delay, in revised budgets, and in the opportunity cost of a stalled initiative. That is what it means to inherit a fraction of someone else’s instability.

Why the Reversal Matters More Than the Restriction

A restriction is a shock. A reversal is a signal. The reversal tells you the rules governing your supply chain are not fixed, they are negotiable, and they will change again. That is the durable takeaway for anyone planning infrastructure over a three-to-five-year horizon.

The distinction matters because organizations respond to shocks and signals very differently. A shock triggers a one-time scramble, after which the natural instinct is to assume the crisis has passed and return to business as usual. A signal, correctly read, changes how you plan permanently. The reversal is the proof that the April restriction was not a one-off event to be absorbed and forgotten. It was one data point in an ongoing pattern of policy volatility that will produce more restrictions, more reversals, and more re-pricing. An IT leader who treats the reversal as good news and moves on has learned nothing. An IT leader who treats it as confirmation that the rules are permanently negotiable has learned the only lesson worth keeping.

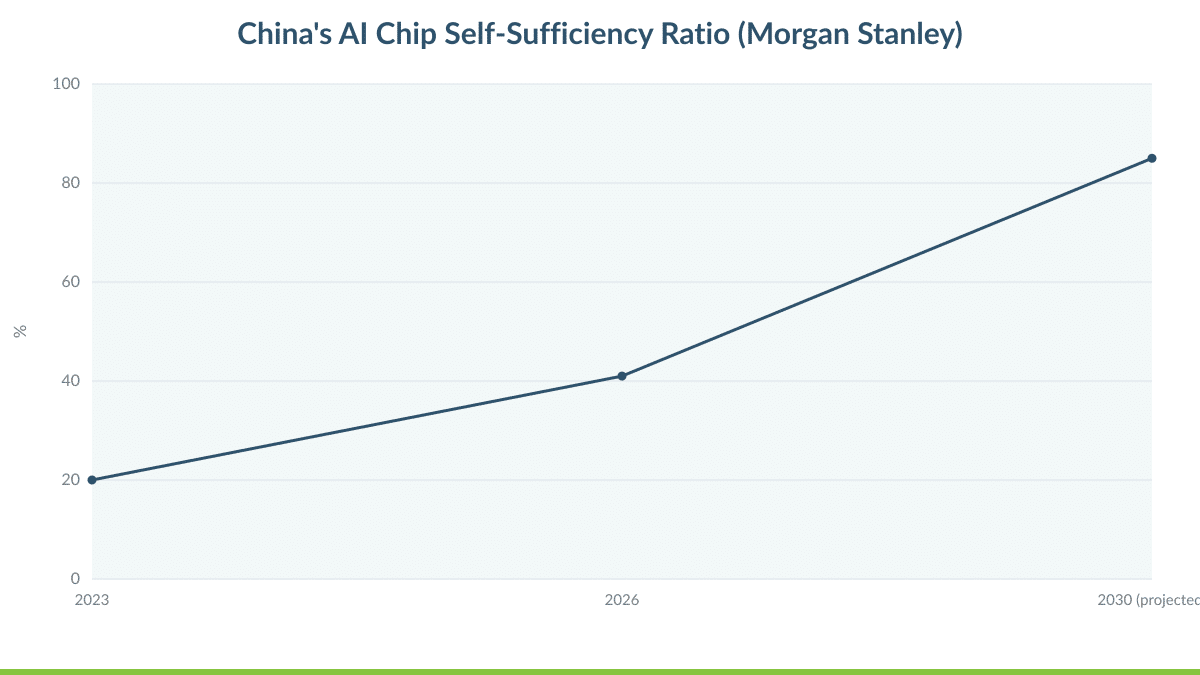

Consider what the reversal reveals about the underlying market dynamics. When the H20 was blocked, China did not stop building AI capability. It accelerated domestic alternatives. Analysts at Morgan Stanley have tracked China’s rising self-sufficiency in AI chips, a trajectory that export controls arguably sped up rather than slowed.

The self-sufficiency curve above, based on Morgan Stanley data, matters to a US mid-market CIO for a specific reason: it demonstrates that supply chains re-route around constraints. When one path closes, capital and engineering flow to alternatives. The vendor you standardized on today may not be the vendor with the most favorable roadmap tomorrow, and the policy that helps a competitor may hurt your incumbent. Building your infrastructure strategy on the assumption that today’s vendor relationships and pricing are permanent is a bet against history.

The re-routing dynamic has a second-order effect that most procurement plans ignore entirely. When a supply chain splits along geopolitical lines, it does not simply produce two parallel versions of the same product. It produces divergence. Standards fork, tooling diverges, and the interoperability you took for granted starts to erode at the margins. A buyer who assumed a single global market for a given class of hardware now navigates a fragmented one, where availability, support, and compatibility vary by region and by policy regime. For a mid-market organization without the scale to hedge across multiple supply paths itself, that fragmentation is a direct threat to the predictability of both cost and capability. This is precisely the kind of complexity that is far better absorbed by a partner operating at scale than shouldered by an internal team.

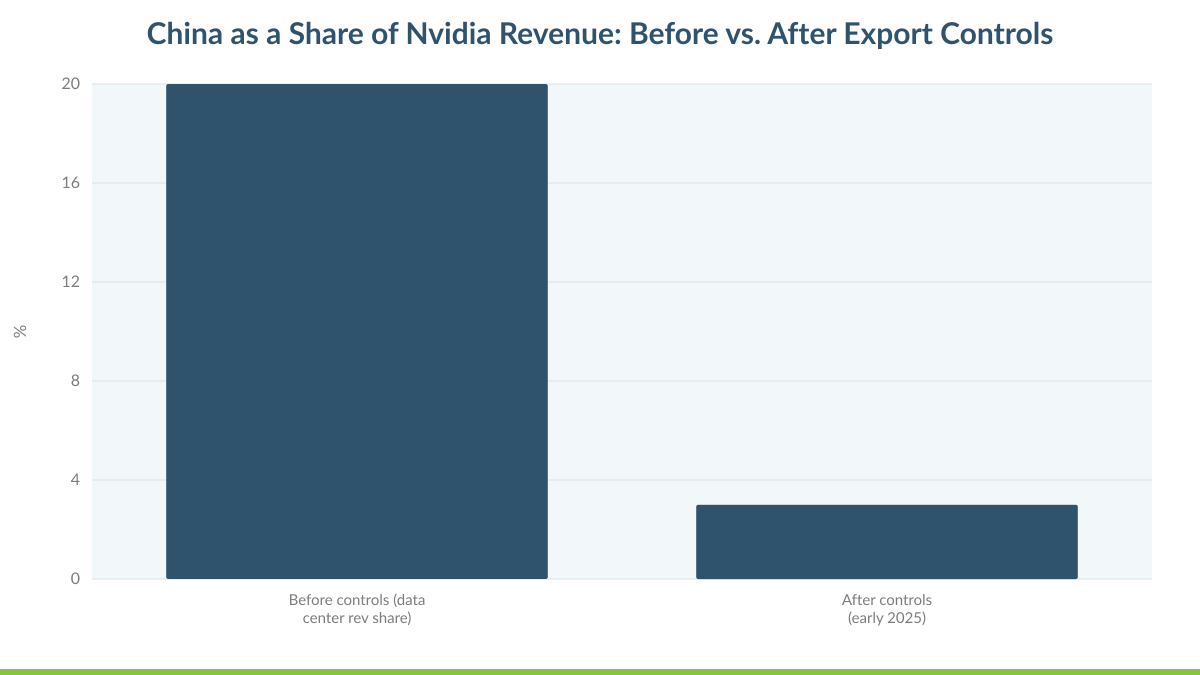

The final chart shows China as a share of Nvidia’s revenue before and after export controls tightened. The decline is the point. A market that once represented a meaningful slice of a dominant vendor’s revenue can shrink dramatically when policy intervenes, and that compression reshapes how the vendor prioritizes everyone else. Product roadmaps, allocation decisions, and support commitments all shift when a major revenue stream is disrupted. You are affected by that reprioritization whether or not you ever touched the restricted product.

Think through the reprioritization concretely. When a vendor loses access to a large revenue stream, it does not absorb the loss passively. It works to recover margin elsewhere, and the levers it pulls are the ones that touch every remaining customer: pricing, bundling, support tiers, and the pace at which older products reach end of support. A vendor under revenue pressure has every incentive to accelerate customers toward higher-margin offerings and to sunset the products that no longer pay their way. The mid-market buyer, who had no involvement in the export decision, discovers that the maintenance renewal costs more, that the entry-level tier has been quietly discontinued, or that the roadmap feature they were waiting on has been deprioritized. The connection between a geopolitical export control and a line item on your renewal invoice is not obvious, but it is real.

A restriction is a shock. A reversal is a signal. The signal is clear: the rules under your infrastructure are negotiable, and they will change again.

The Pattern You Have Already Lived Through

If the AI export restriction feels distant, look closer to home at a policy-driven shock that already reshaped mid-market IT: the Broadcom acquisition of VMware. Overnight, licensing models that had underpinned enterprise virtualization for two decades were rewritten. Perpetual licenses gave way to subscription bundles, minimum core counts changed the math, and organizations that had planned their five-year infrastructure budgets around one pricing structure found themselves recalculating everything.

The parallels are precise. In both cases, a single entity that controls a critical link in the supply chain made a decision that the downstream buyer had no ability to influence and little ability to anticipate. In both cases, the change arrived on the vendor’s timeline, not the customer’s. In both cases, the organizations that had built rigidity into their architecture, whether through single-vendor lock-in or through capital tied up in owned hardware, had the fewest options and the highest costs when the change landed. And in both cases, the event was survivable, even routine, for the organizations that had built flexibility in advance. The VMware transition was not a geopolitical export control, but the mechanism of disruption was identical: a decision outside your control, made by an entity that owns a critical link in your supply chain, that forces you to re-plan on someone else’s timeline.

The organizations that weathered the VMware transition best were not the ones with the largest budgets. They were the ones with flexibility built into their architecture and a partner who could translate a vendor change into a concrete migration plan instead of a panic. A well-funded organization that had committed everything to a single rigid model still faced a costly, disruptive re-architecture. A leaner organization consuming infrastructure as a managed service experienced the licensing change as a conversation about terms rather than a fire drill. Budget did not determine the outcome. Architecture and partnership did.

IT Vortex lived that transition as a Premier Broadcom VCSP Partner. We did not experience the licensing changes as a surprise, we experienced them as a set of decisions to model, price, and route our customers through. That is the difference between a reseller who hands you a quote and an integrator who owns the outcome. When you consume infrastructure through Managed Cloud Hosting instead of owning every layer of the stack, the vendor turbulence becomes our problem to absorb, not yours to survive.

Mapping the AI Export Restriction to Your Five Pillars

Abstract volatility is hard to act on. Concrete pillars are not. Here is how the lessons of the AI export restriction translate into the five dimensions that actually govern mid-market infrastructure decisions.

Flexibility: Do Not Marry a Single Supply Path

The clearest lesson of the H20 saga is that supply paths get cut and re-routed without warning. Flexibility is the direct countermeasure. An architecture that can shift workloads between platforms, absorb a hardware substitution, or move a workload from on-premises to a managed cloud without a ground-up rebuild is an architecture that survives policy shocks. A hybrid cloud model gives you the ability to keep sensitive workloads where you want them while placing burstable or AI-adjacent workloads where the capacity and economics make sense at any given moment.

Flexibility also means not signing procurement contracts that assume the world holds still. When Broadcom changed VMware licensing, the customers who had locked themselves into rigid, single-vendor, single-model commitments had the fewest options. The ones who preserved optionality could pivot. The same principle applies to any AI compute you plan to consume: buy access to capability, not a permanent bet on one silicon supplier. A workload architected to run on a managed platform can follow the most favorable capacity, pricing, and support terms as they shift, rather than being anchored to a depreciating asset that becomes harder to source and support with every policy cycle.

Simplification: Let Someone Else Carry the Complexity

Every layer you own directly is a layer exposed to supply-chain and policy risk. When you own the servers, you own the GPU allocation problem, the lead-time problem, the tariff problem, and the licensing-change problem. When you consume Cloud Hosting (IaaS), those problems become contractual guarantees rather than operational fires. Simplification is not about doing less, it is about pushing the volatile layers onto a partner whose entire business is absorbing that volatility at scale.

There is a hidden cost to owning the volatile layers that rarely appears on a balance sheet: the attention it consumes. Every hour a mid-market IT team spends chasing hardware availability, renegotiating a licensing surprise, or re-planning a refresh around a supply crunch is an hour not spent on the projects that actually differentiate the business. Simplification reclaims that attention. When the volatile layers are contractual guarantees held by a partner, the internal team is freed to focus on applications, data, and the outcomes that move the organization forward. The reduction in operational firefighting is often a larger benefit than the direct cost savings.

This is where the trusted-advisor relationship earns its keep. A good partner does not only sell you capacity but also monitors the vendor landscape, models the impact of announced changes, and brings you a plan before the change hits your budget. That is a fundamentally different service than a transaction.

Performance: Capacity When You Need It, Not Twelve Weeks Later

When AI silicon gets constrained, lead times balloon. A mid-market team trying to buy its own GPU cluster during a supply crunch can wait months for delivery, during which the business case that justified the purchase may evaporate. Consuming performance through a managed platform means the capacity is already provisioned, already supported, and available on demand. You get the performance profile your workload requires without carrying the procurement risk of acquiring and refreshing the underlying hardware yourself.

The timing advantage compounds when you consider how fast the demand curve for AI-adjacent workloads is moving. A business that identifies an analytics or automation opportunity today cannot afford a six-month procurement cycle to test it. By the time the hardware arrives, a competitor operating on managed capacity has already run the experiment, learned from it, and moved on. Speed to capacity is not a convenience, it is a competitive variable. A managed platform turns a multi-month capital procurement into a provisioning decision measured in days, which is the difference between leading a market shift and reacting to it.

Resilience: Assume the Rules Will Change Again

Resilience is the pillar the AI export restriction speaks to most directly. The reversal proved the rules are not stable. Resilient infrastructure is designed on the assumption of future disruption, not the hope of continuity. That means recoverable workloads, tested failover, and data protection that does not depend on any single vendor or facility staying available. Disaster Recovery (DRaaS) and Backup as a Service (BaaS) are the mechanisms that let you treat any single point of failure, supply-driven or otherwise, as a recoverable event rather than an existential one.

Resilience against supply-chain disruption has a dimension that pure cyber resilience does not always capture: the risk of being unable to replace a failed component. In a constrained supply environment, a hardware failure on owned infrastructure is not a same-week fix, it is a wait for allocation. An organization whose workloads are portable and whose data is protected by a service built on Veeam does not depend on the arrival of a replacement part to keep running. The workload moves, the data is intact, and the business continues while the hardware problem is solved on someone else’s timeline. That portability is itself a form of supply-chain insurance.

Resilience planning should be validated, not assumed. A recovery plan that has never been tested is a hypothesis. Regular failover validation turns that hypothesis into a documented capability, and it is the difference between reduce downtime risk with automated recovery workflows and hoping the runbook works when a real incident hits.

Security: Volatility Is a Threat Multiplier

Periods of supply-chain disruption and rushed procurement are exactly when security discipline slips. Teams under pressure to stand up AI capability fast will cut corners, buy gray-market hardware, or deploy workloads without the controls they would normally insist on. That is precisely when attackers benefit. A managed Security as a Service (SECaaS) posture, built on partners like Fortinet, CrowdStrike, and Proofpoint, keeps the security baseline constant even when the procurement environment is chaotic. Security should not be the variable that flexes when supply gets tight.

Gray-market hardware deserves a specific warning, because supply crunches make it tempting. When lead times stretch and a project deadline looms, an unofficial channel promising immediate delivery looks like a solution. It is a trap. Hardware sourced outside authorized channels carries no assurance of firmware integrity, no supply-chain provenance, and no support recourse if it fails. It is exactly the vector a sophisticated attacker would choose to introduce compromised components into a target environment. The discipline to refuse that shortcut is far easier to maintain when the pressure to source hardware yourself has been removed entirely by consuming capacity through a managed, secured platform. Not only does that model deliver the capacity you need but it also eliminates the temptation to compromise your supply-chain integrity under deadline pressure.

What Mid-Market Leaders Should Actually Do

Reading the AI export restriction as a distant headline is a missed opportunity. Reading it as a stress test of your own assumptions is where the value is. Here are the concrete moves that follow from the pattern.

- Audit your single points of vendor dependency. Identify every layer of your stack where a policy change or licensing shift by one vendor would force an unplanned migration, and rank them by business impact.

- Convert fixed hardware bets into consumable capacity where it makes sense, so that supply crunches and lead-time spikes become someone else’s problem to solve at scale.

- Preserve optionality in every procurement contract. Favor terms that let you pivot when a vendor changes its model, as Broadcom did with VMware.

- Test your recovery, do not assume it. Validate failover on a schedule so that any disruption, supply-driven or cyber, is a recoverable event.

- Hold your security baseline constant. Do not let a rush to deploy AI capability erode the controls you would otherwise require.

The dependency audit is the move to start with, because it is the one most organizations skip. Most IT teams can name their vendors, but few have mapped what happens if any one of those vendors changes the rules. The exercise is straightforward: for each critical layer of the stack, ask what a licensing change, an end-of-support announcement, or a supply disruption from that vendor would cost in dollars and in time to remediate. The answers reveal where the real fragility sits, and it is rarely where teams assume. The layer everyone worries about is often well hedged, while the quiet dependency nobody thinks about is the one that would force an emergency re-architecture. Ranking those exposures by business impact turns an anxious sense that “anything could happen” into a prioritized list of what to fix first.

These moves are not exotic. They are the difference between an infrastructure strategy that assumes stability and one that assumes change. The organizations that came through the VMware transition, the Exchange end-of-support deadline, and every prior supply shock in good shape were the ones already operating on the second assumption. You can review how we approach that work across our case studies, and you can pressure-test your own procurement posture against our technology procurement and licensing approach.

An infrastructure strategy that assumes stability is a bet against history. The organizations that thrive assume the rules will change, and build so that change is a routine event, not a crisis.

The Integrator Difference

There is a meaningful gap between a company that sells you technology and a company that owns the outcome of your infrastructure. A reseller passes along whatever the vendor announces, including the surprises. An integrator, architect, and advisor absorbs the vendor turbulence, models its impact, and brings you a plan. When the AI export restriction reversed, when Broadcom rewrote VMware licensing, when Microsoft ended Exchange support, the organizations with the right partner did not experience those as emergencies. They experienced them as scheduled conversations.

The economics of that difference favor a partner operating at scale for a simple reason. A managed cloud provider spreads the cost of monitoring the vendor landscape, negotiating terms, hedging supply, and maintaining engineering depth across a large base of customers. No single mid-market IT department can justify a dedicated function to track export policy, model licensing scenarios, and maintain vendor relationships across the full stack. Consumed as a service, that capability becomes affordable, because you are sharing it. This is the same principle that made cloud computing compelling in the first place, applied to the layer most organizations still try to manage alone: the risk and volatility of the supply chain itself.

Lou Corriero, VP Cloud at IT Vortex, has spent years helping mid-market leaders read exactly these signals and build architectures that do not break when the supply chain gets re-drawn. As a Subject Matter Expert on VMware-powered managed cloud, his focus is not on selling you a product but on designing the platform that makes the next policy shock a non-event for your business. The value is not in predicting which restriction comes next. It is in building infrastructure that does not care.

The AI export restriction and its reversal handed every IT leader a free stress test. The question it asks is simple: if the rules under your infrastructure changed tomorrow, who absorbs the shock, you or your partner? If the honest answer is you, that is the thing worth fixing before the next reversal arrives. Schedule a conversation with Lou Corriero to map your current vendor dependencies against a resilient, flexible cloud architecture, and turn the next supply-chain surprise into a scheduled conversation instead of a scramble.