Across the next 2–3 quarters (Q1–Q3 2026), many organizations should expect continued upward pressure on server and PC hardware pricing. The biggest near-term drivers are not always CPUs or chassis—pricing is being pushed primarily by memory (DRAM) and flash storage (NAND/SSD), compounded by AI-driven demand and procurement volatility.

Executive Summary

- Memory and storage are the primary cost accelerators for servers and modern endpoint builds—especially for virtualization, VDI, and data-heavy workloads.

- AI infrastructure demand is absorbing supply chain capacity and tightening component availability.

- OEM and channel price actions are increasingly showing up in quotes, configuration guidance, and renewal cycles.

- IT leaders should respond with procurement guardrails, architecture efficiency, and budget risk controls—not “wait and see.”

What’s Actually Getting More Expensive (and Why That Matters)

When teams hear “hardware inflation,” they often assume it’s driven by CPUs or servers “in general.” In practice, the cost curve is being shaped most by:

- Server DRAM (RDIMMs/LRDIMMs)

- NAND flash and SSDs

- High-memory configurations (where incremental RAM increases drive outsized cost growth)

- AI-adjacent supply constraints that ripple into standard enterprise server and PC builds

This matters because memory and storage are no longer minor line-items—especially for virtualization clusters, VDI/DaaS, databases, security platforms, and analytics workloads where memory footprints scale quickly.

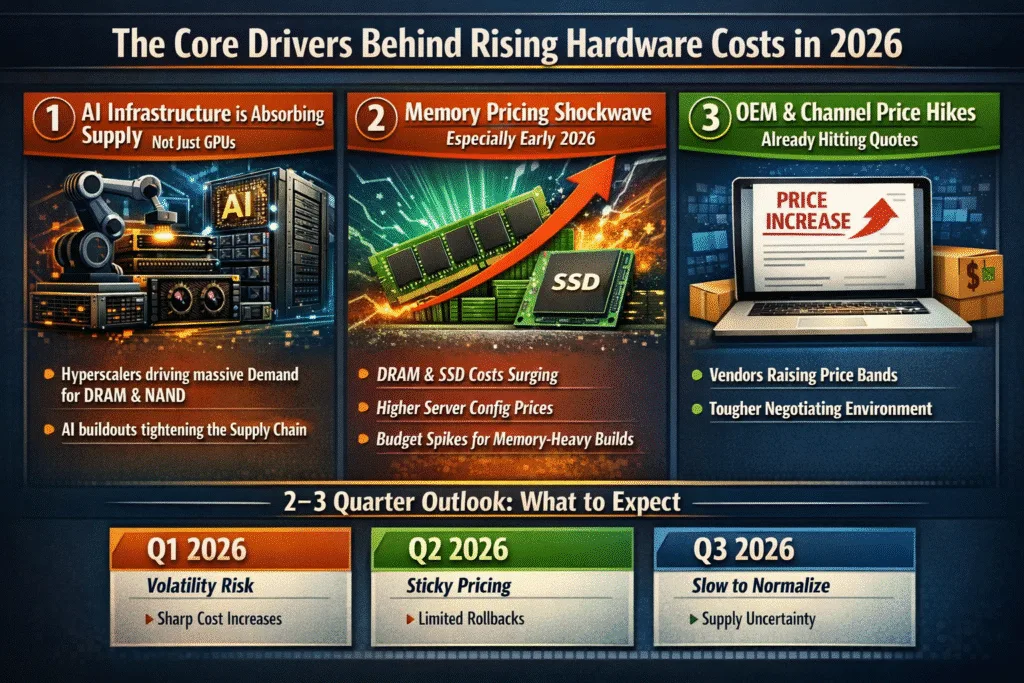

The Core Drivers Behind Rising Hardware Costs in 2026

1) AI Infrastructure Is Absorbing the Supply Chain (Not Just GPUs)

AI buildouts don’t only consume GPUs. They also drive heavy demand for memory and storage, and as hyperscale buyers prioritize supply commitments, broader enterprise procurement can face tighter availability and reduced negotiating leverage.

2) Memory Pricing Is the Near-Term Shockwave (Especially Early 2026)

Market forecasting for early 2026 highlights substantial potential pricing pressure for DRAM and NAND. When DRAM and SSD pricing moves quickly, it tends to show up immediately in: (a) server quotes, (b) recommended configurations, and (c) the total cost of builds sized for modern workloads.

3) OEM and Channel Price Actions Are Already Showing Up

Once OEMs and large channel partners revise pricing bands, prices typically do not revert quickly. Even if underlying component markets soften later, end-customer pricing tends to normalize slowly.

4) Tariff and Policy Uncertainty Can Pull Demand Forward

Even when tariffs are not the sole driver, uncertainty can cause buyers to accelerate purchases to reduce exposure—creating short-term demand spikes and amplifying pricing volatility in the channel.

2–3 Quarter Outlook (Q1–Q3 2026): What to Expect

No forecast is perfect, but a practical planning view for IT leaders is:

Q3 2026: Dependent on whether supply catches up and whether major AI procurement continues to crowd out commodity supply. Budget assuming normalization is slow, not sudden.

Q1 2026: Highest volatility risk. Expect sharper component-driven pricing shifts—especially for memory-heavy server configurations.

Q2 2026: Pricing “stickiness.” Once OEM quoting moves up, reductions tend to lag. Availability constraints may persist depending on hyperscaler and AI-driven demand.

Practical takeaway: If you have refreshes planned in the first half of 2026, treat this as a budgeting and timing risk—not a theoretical issue.

Impact Across the Tech Industry: Who Feels This Most?

Mid-Market IT Teams and MSPs

- More frequent re-quoting and shorter quote-validity windows

- Longer refresh cycles (“life extension” projects)

- Greater pressure to standardize SKUs and reduce bespoke builds

Software and SaaS Vendors

- Higher infrastructure costs—especially for memory-heavy services

- Increased pressure to optimize performance-per-dollar

- Stronger incentives for multi-tenant consolidation and efficient resource allocation

Cloud and Data Center Operators

- Capex increases can influence service pricing over time

- Demand concentration can tighten availability for broader markets

OEMs and Component Manufacturers

- Margin management through packaging and tiering (“good / better / best”)

- Supply allocation dynamics that prioritize large commitments

- Configuration shifts that steer buyers to alternative parts or models

What IT Leaders Should Do Now (Action Plan)

1) Lock Refresh Priorities and Separate “Must-Do” from “Nice-to-Have”

Create two lists:

- Priority A: Security, compliance, uptime, performance bottlenecks

- Priority B: Convenience refreshes, discretionary upgrades

2) Reduce DRAM Exposure with Smarter Architecture Choices

- Right-size virtualization clusters and avoid “just in case” RAM inflation

- Use tiering and workload placement to prevent overbuilding memory footprints

- Rebalance workloads to reduce peak memory demands

3) Build Procurement Guardrails

- Shorten approval cycles for time-sensitive quotes

- Include price-validity windows in project timelines

- Pre-approve alternates (RAM/SSD variants and OEM-equivalent options)

4) Consider Private Cloud as a Financial Hedge

When hardware pricing spikes, consumption-based models can reduce capex shock and stabilize budgeting—especially for:

- VDI / DaaS

- Disaster recovery, backup, and archive

- Seasonal or project-based compute needs

For many organizations, this is the point where private cloud becomes a strategic lever: it converts unpredictable refresh costs into predictable operating expense while keeping governance, performance, and security in enterprise hands.

FAQs

Why are server prices increasing in early 2026?

Pricing pressure is being driven primarily by memory and storage economics and supply-demand imbalances. Memory-heavy configurations are particularly exposed because incremental DRAM adds meaningful cost at scale.

Are PC prices rising for the same reasons?

Often, yes. Endpoint pricing can be influenced by RAM and SSD market conditions, especially for standardized fleets and higher-performance laptop/desktop configurations.

Will prices come down later in 2026?

They can, but enterprise hardware pricing typically normalizes slowly. Even if component markets ease, OEM list and channel pricing often lags downward.

What’s the best way to protect a 2026 IT budget?

Prioritize refreshes, shorten procurement cycles, standardize configurations, improve architecture efficiency, and consider private cloud or managed consumption models where capex volatility is unacceptable.

Want predictability instead of hardware price surprises?

IT Vortex helps organizations stabilize infrastructure costs with VMware-powered private cloud, managed services, and right-sized architecture planning.

Request a 2026 Infrastructure Cost Review and get a refresh plan that accounts for pricing volatility, lifecycle constraints, and workload requirements. Book a Meeting